Introduction

Avoiding the most common personal finance mistakes can save beginners a lot of stress and money. However, many people start managing their finances without realizing the pitfalls that can slow down savings, increase debt, or hurt long-term goals. For instance, skipping budgeting or relying too much on credit can create financial problems quickly.

In this guide, we’ll highlight the top mistakes beginners often make and share practical tips to fix them. By understanding these errors early, you can take control of your money, spend wisely, and build a stronger financial future—without feeling overwhelmed. Moreover, these tips are simple enough to implement even if you are just starting.

What Is Personal Finance?

Personal finance refers to how individuals manage their money in daily life. It includes earning, spending, saving, investing, borrowing, and planning for future financial needs. For example, every financial decision you make—small or large—falls under personal finance. In addition, understanding the basics helps prevent costly mistakes later.

Key areas of personal finance include:

- Income management

- Budgeting and expense control

- Saving and emergency planning

- Debt and credit management

- Long-term financial planning

Understanding personal finance helps you control your money instead of letting money control you. Otherwise, people often make mistakes that lead to debt, missed opportunities, and financial stress. Similarly, learning early gives you a head startPersonal Finance Mistakes toward financial stability.

Why Personal Finance Is Important

Personal finance is important because it helps individuals take control of their money and build a secure future. When people understand how to manage their income, expenses, savings, and investments, they are better prepared to handle both everyday needs and unexpected challenges. Without proper financial planning, it becomes easy to overspend, fall into debt, or struggle during emergencies. Personal finance teaches essential skills such as budgeting, saving regularly, avoiding unnecessary debt, and setting realistic financial goals. Personal Finance Mistakes A well-planned budget allows individuals to track where their money goes each month, helping them reduce wasteful spending and focus on priorities. Saving money is another key part of personal finance, as it creates a safety net for emergencies like mine.

- Helps you live within your means

- Reduces financial stress and anxiety

- Prepares you for emergencies

- Enables you to achieve life goals

- Protects you from debt traps

In short, when you understand personal finance, you make informed decisions instead of emotional ones. Therefore, avoiding common personal finance mistakes early can save years of struggle. Additionally, consistent financial tracking ensures long-term stability.

Avoid – Tips for Beginners

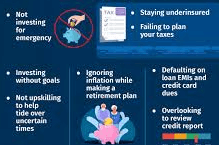

Tip 1: Not Having a Budget

Personal Finance Mistakes to Avoid. One of the biggest personal finance mistakes to avoid is living without a budget. Many beginners spend money without tracking where it goes, which leads to overspending and savings failure. For example, unplanned shopping and impulse purchases can drain your income quickly.

A budget helps you:

- Control unnecessary expenses

- Plan monthly savings

- Understand spending habits

- Avoid living paycheck to paycheck

Even more, without a budget, money disappears fast, and financial goals remain unmet. Therefore, even a simple monthly budget can make a huge difference.

Tip 2: Ignoring Savings and Emergency Funds

Another major mistake is not saving money regularly. Many people believe they will start saving “later,” but later often never comes. As a result, emergencies such as medical bills, job loss, or urgent repairs can create financial stress.

An emergency fund should cover at least three to six months of basic expenses. Without savings, people rely on loans or credit cards, which increases financial pressure. Therefore, saving even a small amount consistently is better than saving nothing. In addition, building an emergency fund early gives you peace of mind.

Tip 3: Relying Too Much on Credit and Loans

Personal Finance Mistakes: Credit cards and loans can be useful; however, when misused, they create long-term financial problems.

Common credit mistakes include:

- Paying only the minimum balance

- Taking loans for unnecessary expenses

- Ignoring interest rates

- Borrowing without a repayment plan

As a result, high-interest debt grows quickly and becomes difficult to manage. In contrast, responsible credit use improves your financial score and borrowing power. Moreover, knowing your interest rates and repayment schedules prevents unnecessary stress.

Tip 4: Not Tracking Expenses

Personal Finance Mistakes: Many people underestimate daily spending. Small costs like subscriptions, coffee, or snacks add up quickly.

Tracking expenses helps you:

- Identify spending leaks

- Reduce unnecessary costs

- Increase savings potential

- Improve budgeting accuracy

In addition, failing to track expenses is one of the most overlooked personal finance mistakes to avoid. Similarly, regular tracking helps you make smarter money decisions.

Tip 5: No Financial Goals

Without clear financial goals, money management becomes directionless. Beginners often focus on short-term needs and ignore long-term planning.

Financial goals can include:

- Saving for emergencies

- Paying off debt

- Buying a home

- Retirement planning

Similarly, setting realistic goals keeps you motivated and disciplined. Furthermore, achieving small milestones builds confidence for larger goals.

Tip 6: Delaying Financial Education

Avoiding money education is a common beginner mistake. However, this leads to repeated errors and missed opportunities.

Learning basics helps you:

- Understand interest and inflation

- Make smarter spending decisions

- Avoid financial scams

- Plan confidently for the future

In short, not learning about money is a dangerous mistake. Additionally, small efforts like reading blogs or books can make a big difference over time.

Tip 7: Lifestyle Inflation

Lifestyle inflation occurs when expenses rise with income. Instead, focus on saving more before upgrading your lifestyle.

Examples include:

- Buying expensive gadgets unnecessarily

- Increasing luxury spending

- Upgrading housing too early

While enjoying income growth is normal, on the other hand, uncontrolled lifestyle inflation prevents wealth building. Therefore, plan upgrades carefully.

Tip 8: Ignoring Long-Term Planning

Beginners often ignore future responsibilities such as retirement, healthcare, or family planning.

Ignoring long-term planning leads to:

- Financial stress later in life

- Dependence on others

- Limited financial freedom

Therefore, thinking ahead is essential. Moreover, early planning allows you to benefit from compound growth and tax advantages.

Common Mistakes Summary

Personal Finance Mistakes to Avoid: Beginners should avoid:

- Spending without planning

- Not saving regularly

- Misusing credit

- Ignoring financial education

- Avoiding long-term planning

- Living beyond means

In addition, avoiding these mistakes requires discipline, awareness, and consistency, not high income.

FAQs

What are the most common personal finance mistakes?

Mistakes include not budgeting, failing to save, relying too much on credit, and ignoring financial education. Furthermore, tracking expenses is also crucial.

Can beginners fix personal finance mistakes?

Yes, beginners can fix mistakes by budgeting, saving consistently, and reducing unnecessary debt. Similarly, fixing small errors early prevents bigger issues.

How can I avoid mistakes early?

Start with budgeting, tracking expenses, building an emergency fund, and learning continuously. Moreover, set realistic goals to guide your decisions.

Is personal finance only about saving?

No, it includes earning, spending, saving, borrowing, and planning. In addition, saving is just one part of financial management.

Conclusion

Personal finance mistakes are not complicated; however, they require awareness and discipline. Most financial problems stem from repeated small errors rather than from a single big decision. By understanding budgeting, saving, credit management, and planning, beginners can build a strong financial foundation.

As a result, avoiding these mistakes allows you to control your money, reduce stress, and achieve goals confidently. Personal finance is a lifelong skill, and therefore, the earlier you master it, the better your financial life. Furthermore, consistent action ensures long-term success.